Parent PLUS Loan repayment begins after the loan is fully disbursed. Typically, this means repayment starts 60 days after the final disbursement.

Parent PLUS Loans are designed to help parents pay for their child’s education. Understanding the repayment timeline is crucial. It helps parents plan their finances effectively. Knowing when the first payment is due can reduce stress. It also helps avoid missed payments.

Parents can choose to defer payments while the student is in school. But interest will still accrue. Knowing these details can make managing the loan easier. This blog will provide all the essential information about Parent PLUS Loan repayment. Stay with us to learn more.

Introduction To Parent Plus Loans

Parent Plus Loans are federal loans available to parents of dependent undergraduate students. These loans help cover education costs not met by other financial aid. They offer a way for parents to support their children’s education without straining their finances.

What They Are

Parent Plus Loans are part of the federal Direct Loan Program. These loans are offered by the U.S. Department of Education. They carry a fixed interest rate and flexible repayment options. They are designed to cover the full cost of a student’s education, minus any other financial aid received.

Who Qualifies

To qualify for a Parent Plus Loan, parents must meet certain criteria:

- The borrower must be the biological or adoptive parent of a dependent undergraduate student.

- In some cases, a stepparent may qualify.

- The student must be enrolled at least half-time in an eligible school.

- The borrower must not have an adverse credit history.

- The borrower and the student must be U.S. citizens or eligible noncitizens.

These loans do not have income limits or require a credit score check. However, a credit check is conducted to ensure the borrower does not have adverse credit.

Application Process

Understanding the application process for a Parent PLUS Loan is essential. This section breaks down the steps, approval criteria, and necessary information.

Steps To Apply

Applying for a Parent PLUS Loan involves several clear steps. Here’s a simple breakdown:

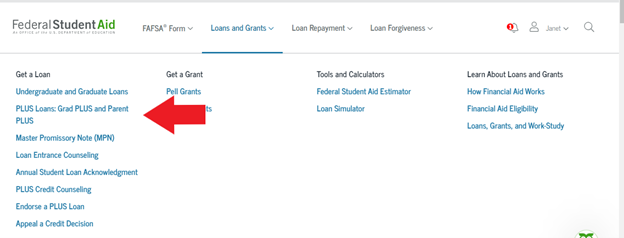

- Complete the FAFSA: Fill out the Free Application for Federal Student Aid (FAFSA).

- Log in to the StudentAid.gov: Use your FSA ID to log in.

- Select the Parent PLUS Loan: Choose the loan option and provide the required information.

- Credit Check: Consent to a credit check by the Department of Education.

- Sign the Master Promissory Note (MPN): Agree to the loan terms by signing the MPN.

Approval Criteria

The approval criteria for a Parent PLUS Loan are straightforward but important. Here’s what you need to know:

- Credit Check: A credit check is required. The applicant must not have an adverse credit history.

- Citizenship: The applicant must be a U.S. citizen or an eligible non-citizen.

- Dependent Student: The loan is for parents of dependent undergraduate students.

If the credit check is unsuccessful, you can appeal or provide an endorser.

Loan Disbursement

Understanding when Parent Plus Loan repayment begins starts with knowing about loan disbursement. Disbursement is the process where the loan funds are released to the school. This helps cover tuition, fees, and other expenses. Here’s a closer look at how this process works.

How Funds Are Released

Once a Parent Plus Loan is approved, the funds go directly to the school. The school first uses these funds to pay for tuition and other school charges. Any remaining funds are then given to the parent or student for other education-related expenses.

Timeline Of Disbursement

The timeline for disbursement can vary. Typically, the school receives the funds at the beginning of each term. This means if your child is enrolled in a program with multiple terms, you might see multiple disbursements.

| Term | Disbursement Timing |

|---|---|

| Fall | Early September |

| Spring | Early January |

| Summer | Early May |

If there are any leftover funds, they are usually released within 14 days after the school applies them to the tuition.

Understanding these timelines helps you prepare for when repayment starts. Stay aware of these dates to manage your finances better.

Credit: osfa.illinois.edu

Repayment Start Date

Understanding the repayment start date of a Parent PLUS Loan is crucial for managing finances effectively. Knowing when the first payment is due helps in planning the budget accordingly. Let’s dive into the details about the repayment start date.

Standard Repayment Schedule

The standard repayment schedule for a Parent PLUS Loan begins right after the loan is fully disbursed. This means as soon as the school receives the last portion of the loan funds, repayment starts. Typically, parents have a six-month grace period before the first payment is due. During this time, it’s wise to prepare for the upcoming financial commitment.

Deferment Options

If immediate repayment is a concern, there are deferment options available. Parents can request to defer payments while the student is enrolled at least half-time, and for an additional six months after the student graduates or drops below half-time enrollment. Interest, however, continues to accrue during this period, which can increase the total amount owed.

| Repayment Start Date | Conditions |

|---|---|

| Immediate | After loan disbursement |

| Deferment | While student is enrolled and six months post-enrollment |

Being aware of these timelines and options allows for better financial planning. Make informed decisions about your repayment strategy.

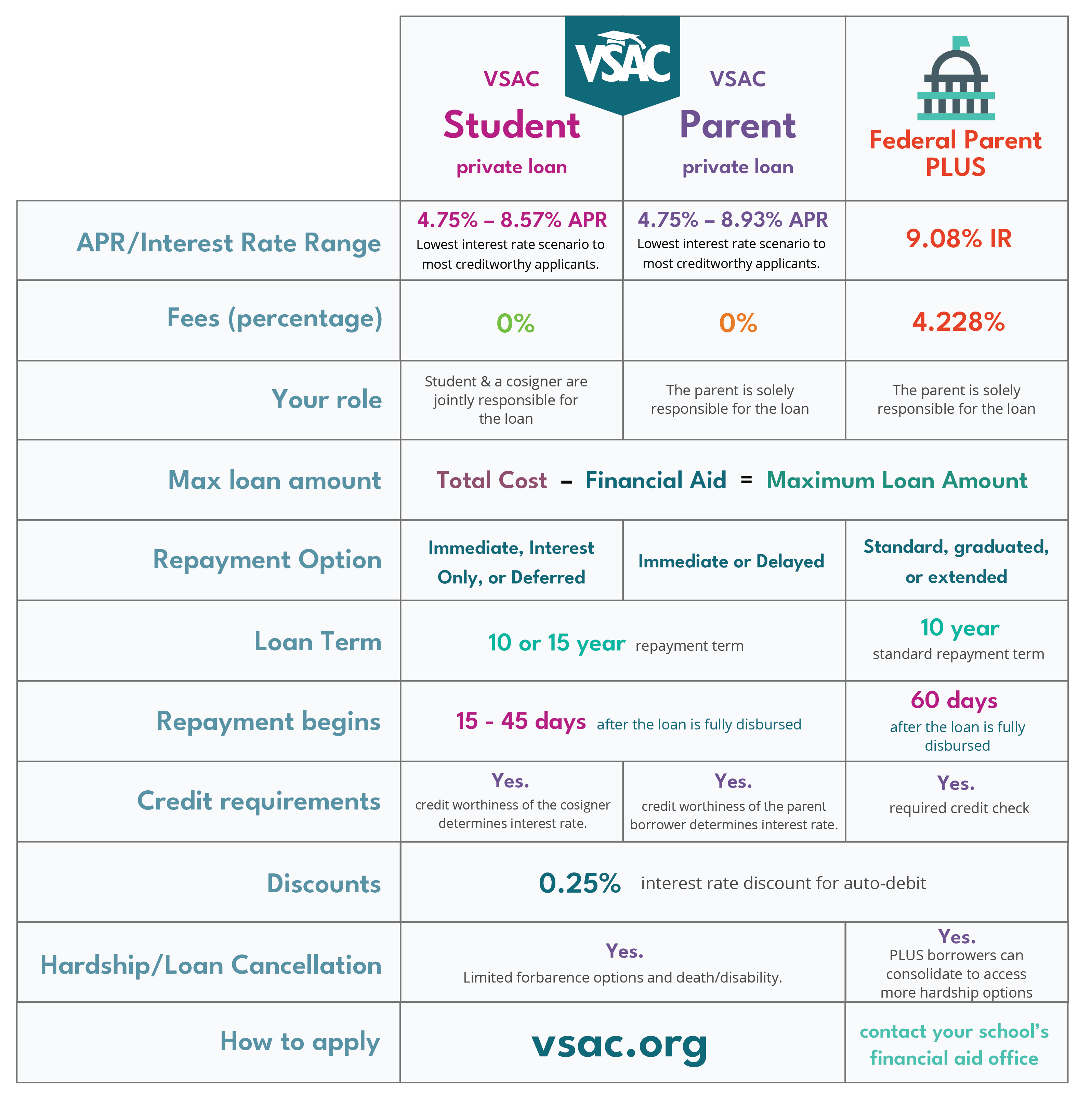

Repayment Plans

Understanding the repayment plans for Parent PLUS Loans is crucial. Parents need to know their options to manage their finances effectively. This section will cover the available plans and help you choose the right one.

Available Options

There are several repayment plans for Parent PLUS Loans. Each plan offers different benefits. Here are the primary options:

- Standard Repayment Plan: Fixed monthly payments for up to 10 years.

- Graduated Repayment Plan: Payments start low and increase every two years, up to 10 years.

- Extended Repayment Plan: Fixed or graduated payments for up to 25 years.

- Income-Contingent Repayment (ICR) Plan: Payments are based on your income and family size, up to 25 years.

Choosing The Right Plan

Choosing the right repayment plan depends on your financial situation. Here are some factors to consider:

- Monthly Budget: Calculate your monthly expenses. Choose a plan that fits your budget.

- Loan Amount: Larger loans may benefit from extended or graduated plans.

- Income Stability: If your income varies, an income-contingent plan might be best.

- Repayment Term: Shorter terms save on interest but have higher payments. Longer terms lower monthly payments but increase total interest.

Each plan has its pros and cons. Evaluate each option carefully to make the best decision for your financial future.

Credit: studentaid.gov

Managing Repayment

Managing Parent Plus Loan repayment can seem overwhelming at first. But with the right strategies, it becomes manageable. This section will guide you on how to handle your repayment efficiently. We’ll cover essential tips for budgeting and ways to deal with payment challenges.

Budgeting Tips

Creating a budget is crucial for managing your loan repayment. Here are some tips to help you stay on track:

- Track Your Spending: Note down all your expenses. This helps identify areas where you can cut costs.

- Create a Repayment Plan: Allocate a specific amount for your loan repayment each month. Stick to this plan.

- Prioritize Payments: Pay your loan before other less critical expenses. This ensures you avoid late fees.

- Use Budgeting Tools: Utilize apps and tools to keep track of your budget. These tools can simplify the process.

Handling Payment Challenges

Facing difficulties with loan repayment? Here are some strategies to consider:

- Contact Your Loan Servicer: Explain your situation. They might offer solutions like deferment or forbearance.

- Explore Income-Driven Repayment Plans: These plans adjust your monthly payment based on your income. This can make payments more manageable.

- Seek Financial Counseling: A financial counselor can help you create a plan to manage your repayments. They offer valuable advice and support.

- Consider Loan Consolidation: Combining multiple loans into one can simplify your payments. It might also lower your interest rate.

By following these tips, you can successfully manage your Parent Plus Loan repayment. Remember, staying organized and seeking help when needed can make a big difference.

Credit: www.vsac.org

Frequently Asked Questions

When Does Parent Plus Loan Repayment Start?

Repayment starts after the loan is fully disbursed. Usually, this is after the spring semester ends.

Can Parent Plus Loan Repayment Be Deferred?

Yes, you can defer repayment while your child is in school. You must request this from your loan servicer.

How Long Is The Grace Period For Parent Plus Loans?

There is no grace period. Repayment starts 60 days after the loan is fully disbursed.

Are There Repayment Plans For Parent Plus Loans?

Yes, various plans are available. These include standard, graduated, and extended repayment plans.

Can Parent Plus Loans Be Consolidated?

Yes, you can consolidate Parent PLUS loans. This may simplify payments and extend repayment terms.

Conclusion

Repaying a Parent PLUS Loan can seem daunting, but it’s manageable. Remember, repayment starts six months after your child leaves school. Planning ahead helps you stay on track. Create a budget and explore repayment options. Stay informed about deadlines and terms.

This ensures a smoother repayment journey. Seek assistance if needed. Many resources offer help. Being proactive makes the process easier.