A Parent PLUS Loan is due once the loan is fully disbursed. Payments start 60 days after the final disbursement.

Understanding the due date for a Parent PLUS Loan is crucial for planning. These loans help parents cover their child’s education costs. But knowing when payments start can prevent financial surprises. Parent PLUS Loans offer flexibility but come with specific repayment terms.

This blog will explain when payments begin and what options parents have. We’ll also discuss ways to manage these loans effectively. Understanding these details can ease the burden of repayment. Let’s dive into the key information every parent borrower needs to know.

Introduction To Parent Plus Loans

Parent PLUS Loans are a popular option for parents to help pay for their child’s college education. These loans are offered by the federal government and can cover the cost of tuition, room, board, and other expenses. Understanding the details of Parent PLUS Loans is crucial for making informed financial decisions.

What Are Parent Plus Loans?

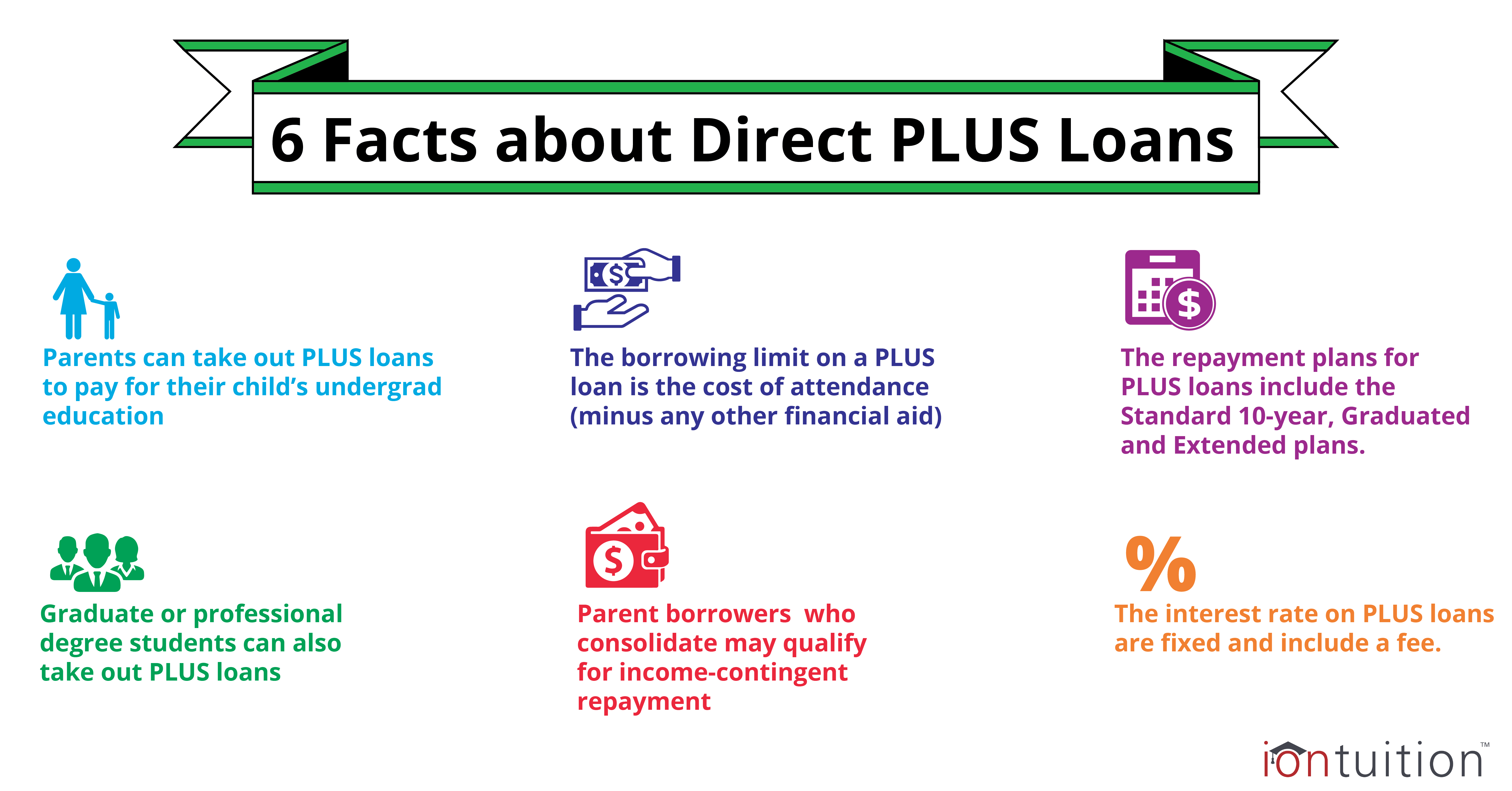

Parent PLUS Loans are federal loans that parents can use to help pay for their child’s education. The loans are available to parents of dependent undergraduate students. Unlike other federal student loans, the parent is responsible for repaying the loan, not the student.

Benefits Of Parent Plus Loans

- Flexible loan amounts: Parents can borrow up to the total cost of attendance, minus any other financial aid the student receives.

- Fixed interest rate: Parent PLUS Loans have a fixed interest rate, which means the rate will not change over the life of the loan.

- Deferment options: Parents can defer payments while their child is in school and for six months after graduation.

- Loan forgiveness: In some cases, Parent PLUS Loans may be eligible for loan forgiveness programs.

Credit: www.iontuition.com

Loan Repayment Timeline

Understanding the loan repayment timeline for Parent PLUS Loans is crucial. Knowing when payments start can help parents plan their finances better. Let’s break down the timeline.

When Repayment Begins

Repayment for Parent PLUS Loans begins after the loan is fully disbursed. This means once the loan amount is sent to the school, repayment starts. Borrowers need to be prepared for this.

Grace Period Details

Parent PLUS Loans offer a six-month grace period. This period starts after the student graduates, leaves school, or drops below half-time enrollment. During this time, no payments are required.

| Event | Repayment Start |

|---|---|

| Loan Disbursement | Immediately |

| Student Graduation | Six months after |

| Leaving School | Six months after |

| Dropping Below Half-Time | Six months after |

During the grace period, interest will accrue. Borrowers can choose to pay interest during this time. This can prevent interest from being added to the principal balance.

Understanding these details can help parents manage their finances and avoid surprises.

Repayment Plan Options

Understanding the repayment plan options for Parent PLUS Loans can help you manage your finances better. Here, we will explore two main options: the Standard Repayment Plan and the Income-Contingent Repayment Plan.

Standard Repayment Plan

The Standard Repayment Plan is straightforward. You make fixed monthly payments over a set period. Typically, this period is ten years. Monthly payments are higher, but you pay less interest over time. This plan is ideal if you can afford higher monthly payments.

| Feature | Details |

|---|---|

| Monthly Payment | Fixed |

| Repayment Term | 10 years |

| Interest Paid | Lower over time |

Income-contingent Repayment Plan

The Income-Contingent Repayment Plan (ICR) adjusts your monthly payments based on your income. This can be helpful if you have a lower income. Payments can be as low as $5 per month. The repayment term can extend up to 25 years. After 25 years, any remaining loan balance may be forgiven.

- Payments based on income and family size

- Repayment term up to 25 years

- Possibility of loan forgiveness after 25 years

Choosing the right plan can make a big difference. Consider your financial situation and long-term goals. This way, you can select the best repayment plan for your needs.

Credit: financialaid.sfsu.edu

Deferment And Forbearance

Understanding the repayment options for a Parent Plus Loan is crucial. Two common options are deferment and forbearance. These options offer temporary relief when you cannot make payments.

Eligibility For Deferment

Deferment allows you to temporarily stop making payments on your loan. Not everyone qualifies for deferment. You must meet specific criteria.

- Enrollment: The student must be enrolled at least half-time at an eligible school.

- Unemployment: If you are unemployed, you may qualify.

- Economic Hardship: Demonstrating financial difficulty can make you eligible.

During deferment, interest may still accrue. But you won’t need to make payments. Check if you meet the criteria before applying.

How Forbearance Works

Forbearance is another option to pause or reduce loan payments. Unlike deferment, forbearance is available if you do not qualify for deferment.

There are two types of forbearance: general and mandatory.

| Type | Details |

|---|---|

| General Forbearance | Granted for financial difficulties, medical expenses, or changes in employment. |

| Mandatory Forbearance | Required if you meet specific conditions, like serving in a medical or dental internship. |

Interest accrues during forbearance. You can choose to pay the interest or let it capitalize. Paying the interest can save you money in the long run.

Strategies For Managing Payments

Managing payments for a Parent Plus Loan can feel overwhelming. However, with the right strategies, you can stay on track and maintain financial stability. Below are some effective methods to help you manage your Parent Plus Loan payments efficiently.

Creating A Budget

Creating a budget is essential for managing your loan payments. Start by listing all your income sources and monthly expenses. This helps you understand where your money goes.

Here’s a simple way to create a budget:

- Write down your total monthly income

- List all your fixed expenses (rent, utilities, etc.)

- Include variable expenses (groceries, entertainment, etc.)

- Subtract your expenses from your income

If you have a surplus, allocate a portion to your loan payments. This helps reduce the loan balance faster. If you have a deficit, identify areas to cut back on spending.

Automatic Payments

Setting up automatic payments can simplify the process. Many loan servicers offer this feature. It ensures your payments are on time every month.

Here are the steps to set up automatic payments:

- Log in to your loan servicer’s website

- Navigate to the payment options section

- Select automatic payments

- Enter your bank account details

- Choose your payment date

Automatic payments can also help you avoid late fees. Some servicers even offer interest rate discounts for using this option.

By implementing these strategies, you can manage your Parent Plus Loan payments effectively and reduce financial stress.

Credit: www.edvisors.com

Consequences Of Default

Defaulting on a Parent PLUS Loan can have serious consequences. It affects your financial health and can lead to stressful collection actions. Understanding the potential impacts can help you avoid these pitfalls.

Impact On Credit Score

Defaulting on a loan significantly damages your credit score. A lower credit score means higher interest rates on future loans. It can also affect your ability to rent an apartment or buy a car.

| Credit Score Range | Possible Effects |

|---|---|

| Excellent (800-850) | Minimal impact, but still noticeable |

| Good (700-799) | Greater impact, noticeable drop |

| Fair (650-699) | Significant impact, hard to recover |

| Poor (600-649) | Severe impact, major financial hurdles |

| Very Poor (300-599) | Extreme impact, few options left |

Collection Actions

When you default on a Parent PLUS Loan, the government can take collection actions. These actions can include wage garnishment. This means they take money directly from your paycheck.

They can also withhold tax refunds. The IRS will take your tax refund to pay the loan.

Another consequence is the loss of eligibility for new federal student aid. This means you can’t get more loans to help your children with their education.

- Wage Garnishment: Direct deductions from your paycheck.

- Tax Refund Withholding: The IRS uses your refund to pay the loan.

- Loss of Aid Eligibility: No new federal student loans.

In summary, avoiding default on a Parent PLUS Loan is crucial. The consequences are far-reaching and can affect your financial future. Stay informed and proactive to manage your loans effectively.

Frequently Asked Questions

When Is A Parent Plus Loan Due?

Parent Plus Loans are due after disbursement. Repayment starts 60 days later.

Can I Defer Parent Plus Loan Payments?

Yes, you can request deferment while your child is in school. Interest accrues during deferment.

How Long Is The Repayment Period For Parent Plus Loans?

The standard repayment period is 10 years. Other repayment plans may extend it.

Are Parent Plus Loan Payments Flexible?

Yes, flexible repayment plans are available. Examples include Income-Contingent Repayment and Graduated Repayment.

What Happens If I Miss A Parent Plus Loan Payment?

Missed payments can result in late fees. It may also affect your credit score.

Conclusion

Knowing when a Parent PLUS Loan is due helps you plan better. Timely payments avoid extra charges and interest. Check your loan servicer’s website for exact dates. Stay organized and set reminders for payment deadlines. This keeps your credit score healthy.

Remember, understanding your loan terms is key. It makes managing finances easier. Parents can then focus on supporting their child’s education. Financial peace of mind is achievable with the right information. Stay informed and proactive.